In "U.S. Shale Oil Revolution & Future," Will Reese explores the transformative impact of the shale oil revolution on the U.S. energy sector and its broader geopolitical implications. The article highlights the pivotal role of technological advancements in horizontal drilling and multi-stage fracking, which revived U.S. natural gas and shale oil production starting in 2007.

Horizontal drilling and fracking techniques significantly reduced the breakeven price for shale oil, from $75-$85 per barrel to $35-$45 per barrel. This innovation frustrated OPEC and Russia, leading them to adjust their production strategies. U.S. shale production grew rapidly, turning the country into a leading oil producer and reducing dependency on foreign oil.

Despite past successes, major shale basins like Eagle Ford and Bakken are showing signs of exhaustion. The Permian Basin remains a key growth area but cannot sustain its current growth indefinitely. Production stagnated in 2021 and 2022 despite higher oil prices, signaling potential future declines.

Encourage Upstream Investment: Promote drilling, infrastructure development, and federal lease bidding to avoid peak oil supply declines.

Private Equity Involvement: Increase capital expenditures through private equity firms to fill funding gaps left by large banks and asset managers.

Innovative Extraction Techniques: Use enhanced oil recovery methods, such as gas injection, to extend the life of older wells and boost production.

Tax Incentives: Restore the 15% tax credit for enhanced oil recovery to incentivize investment in advanced extraction technologies.

Reese emphasizes the importance of energy-friendly policies and balanced environmental regulations to sustain the industry's growth. Radical ESG initiatives from international bodies should be carefully considered to avoid economic disruptions.

The U.S. shale oil revolution has significantly bolstered the nation's energy independence and economic stability. Continued investment, technological innovation, and supportive policies are crucial for maintaining growth and addressing future challenges. The Financial Policy Council (FPC) plays a vital role in advocating for policies that support the industry's stability and growth.

For more information, visit Financial Policy Council.

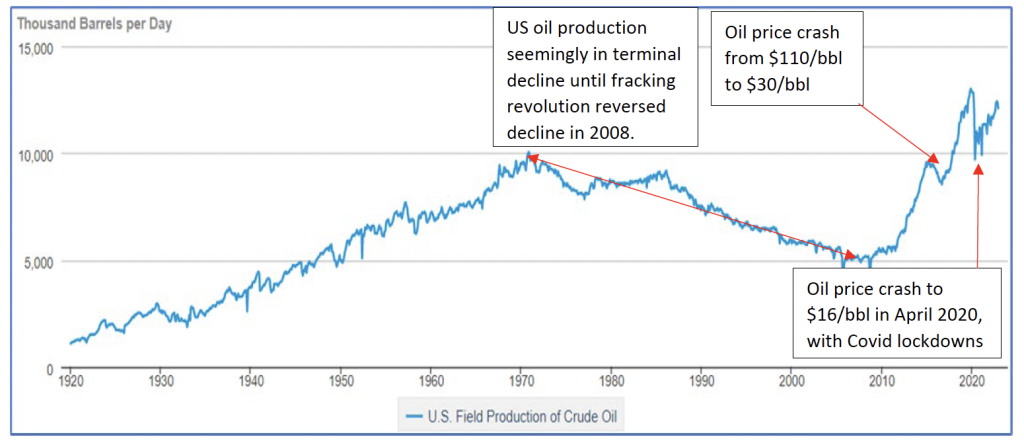

From the 1970’s the concerns about fossil fuel-based economies were based on peak oil which is the hypothetical point in time when the maximum rate of global oil production is reached. During the 1970s, the peak oil theory seemed plausible in the United States, and many believed that global peak oil was inevitable. However, in 2007, the introduction of horizontal drilling and multi-stage fracking revived US natural gas production, and these techniques were soon replicated in shale oil basins. As a result, in 2008, onshore shale oil production flattened the decline, and by 2012, it had significantly reversed, as seen in the graph below.

It took high oil prices to spur the shale oil revolution with oil prices ranging from $80-$110/bbl. This was universally viewed as necessary to fuel the shale expansion with most Exploration and Production (E&P) companies like ExxonMobil, Chevron and British Petroleum requiring an average breakeven price of ~$75-$85/bbl. The rapid expansion of onshore shale oil, long lead deepwater projects(1) coming online and Saudi Arabia ramping up production led to the world entering an unthinkable glut of oil. It was predicted that shale production would die off due to the high-cost nature of the business until shale producers took a more disciplined approach to identifying the sweet spots, improving drilling rates, and fracturing technologies which reduced their breakeven price to $35-$45/bbl. This frustrated OPEC and Russia which attempted to crush shale oil by flooding the world with cheap crude oil and eventually reversed course in 2017 by cutting oil production to support oil prices. This shift in strategy highlights the impact that advancements in shale production have had on the global oil market, forcing major oil-producing countries to reconsider their tactics to maintain market share and influence. Moreover, the growth of the shale industry has contributed to the diversification of global energy sources, increasing competition in the market and prompting countries like OPEC and Russia to adapt their strategies accordingly.

As U.S. shale producers successfully lowered their costs, various politicians claimed credit for this achievement, despite either opposing or genuinely supporting the industry. Recognition should be given to those politicians who implement energy-friendly policies that enable oil producers to excel while maintaining safety and environmentally-friendly practices at the most reasonable levels. However, it’s essential to understand that no single politician can genuinely claim sole responsibility for this success. Although it’s understandable that politicians present an optimistic view of their capabilities to win elections, the industry’s accomplishments and long-term energy security shouldn’t be taken for granted. Complacency could lead to a recurrence of the energy crisis experienced by the U.S. and the world in 2008, prior to the fracking revolution which led to a shift in consumer behavior, with people seeking out more fuel-efficient vehicles and adopting energy-saving measures to reduce their reliance on expensive energy sources with businesses adapting by improving energy efficiency, seeking out alternative energy sources, and adopting cost-cutting measures to remain competitive.

There are already signs that major shale basins that boomed in the previous decade are starting to show signs of exhaustion such as the Eagle Ford in South Texas and Bakken shale in North Dakota, Montana, and the Canadian province of Saskatchewan.

During 2021 and 2022, the Bakken and Eagle Ford production remained stagnant, even though oil prices were higher ($71 and $101 per barrel, respectively) compared to the average oil prices of $54 and $71 per barrel in 2018 and 2019 when the Bakken and Eagle Ford production increased significantly.

This leaves the Permian basin located in the southwestern United States, primarily in West Texas and southeastern New Mexico as the only major US basin with growth ahead in future years, but even the Permian basin cannot maintain this level of growth indefinitely. Earlier this month, the Energy Information Administration (EIA) forecast that oil production in the United States would grow by 590,000 barrels per day (bpd) to a total of 12.44 million bpd. The statement also mentioned that in 2024, production growth is expected to be only 90,000 bpd by those within the industry. “The aggressive growth era of US shale is over,” Scott Sheffield, the chief executive of Pioneer Natural Resources, the top shale independent in the country, told the Financial Times in January. “The shale model definitely is no longer a swing producer” having lost its ability to quickly adjust its oil production in response to changes in global oil prices or market conditions, thus no longer playing the same influential role in the global oil market as it once did.

The shale revolution has significantly impacted the United States and its consumers while posing challenges for geopolitical adversaries like Russia and OPEC countries. The shale industry’s short cycle time, minimal exploration costs, and low risk for adding new production have contributed to a decrease in industry capital expenditure from approximately $1.23 trillion/year in 2011-2014 to around $0.91 trillion/year between 2015 and 2022. However, there is a silver lining, as industry capital expenditure is projected to reach $1.15 trillion in 2023.

It is critical that the radical ideas such crippling the industry through ESG from elites in Davos and the UN be rejected at all costs in order to protect the sector’s continued growth and stability. This is because the oil and gas industry is a significant contributor to the global economy and energy security, and sudden disruptions could lead to economic downturns, job losses, and geopolitical tensions. Energy diversification by expanding multiple sources is necessary which can include clean & lower carbon sources provided consistent baseload power is not neglected. This will allow for innovation and the integration of new technologies while maintaining a stable energy supply. By adopting a more balanced approach, stakeholders can address environmental concerns without jeopardizing the industry’s critical role in the global economy and in international relations.

Upstream investment such as drilling wells, constructing pipelines, and developing infrastructure to support the extraction in both exploration and production should be encouraged by aggressively opening new federal lease bidding in the United States and around the globe to avoid peak domestic oil supplies in the not-too-distant future where the production of oil reaches its maximum level and begins to decline.

Below are my recommendations for ways to ensure that the industry has the necessary capital and technical solutions to address these challenges.

In conclusion, the Financial Policy Council with its robust member representation in the Oil and Gas silos plays an important current and future role in the US shale and oil revolution and has been at the forefront of change by providing important tax policy recommendations that support the industry’s growth and stability while addressing environmental concerns. The FPC advocates for opening new federal lease bidding in the United States and around the globe to avoid peak domestic oil supplies and advocates policies that encourage upstream investment, such as drilling wells, constructing pipelines, and developing infrastructure to support the extraction in both exploration and production.

Sign up now and join the conversation at https://financialpolicycouncil.org/blog/.

Disclaimer: This article discusses certain companies and their products or services as potential solutions. These mentions are for illustrative purposes only and should not be interpreted as endorsements or investment recommendations. All investment strategies carry inherent risks, and it is imperative that readers conduct their own independent research and seek advice from qualified investment professionals tailored to their specific financial circumstances before making any investment decisions.

The content provided here does not constitute personalized investment advice. Decisions to invest or engage with any securities or financial products mentioned in this article should only be made after consulting with a qualified financial advisor, considering your investment objectives and risk tolerance. The author assumes no responsibility for any financial losses or other consequences resulting directly or indirectly from the use of the content of this article.

As with any financial decision, thorough investigation and caution are advised before making investment decisions.

Introduction: A State Betrayed by Greed Florida, the sun-soaked paradise where retirees come to enjoy their golden years, where families build their futures, where millions...

Martin C. Johns MD

Martin C. Johns MD The Dawn of the AI-Driven Property Wars: A Revolution Beyond the Realm of Human Comprehension The integration of artificial intelligence into real estate is not...

Karina Benzineb

Karina Benzineb DECLASSIFY ZERO POINT ENERGY TECHNOLOGY TO THE WORLD Let us delve into the history of science, specifically the science behind innovative energy creation. While Alternative...

Jasmine Bingham

Jasmine Bingham We Extend Our Gratitude to Our Partners